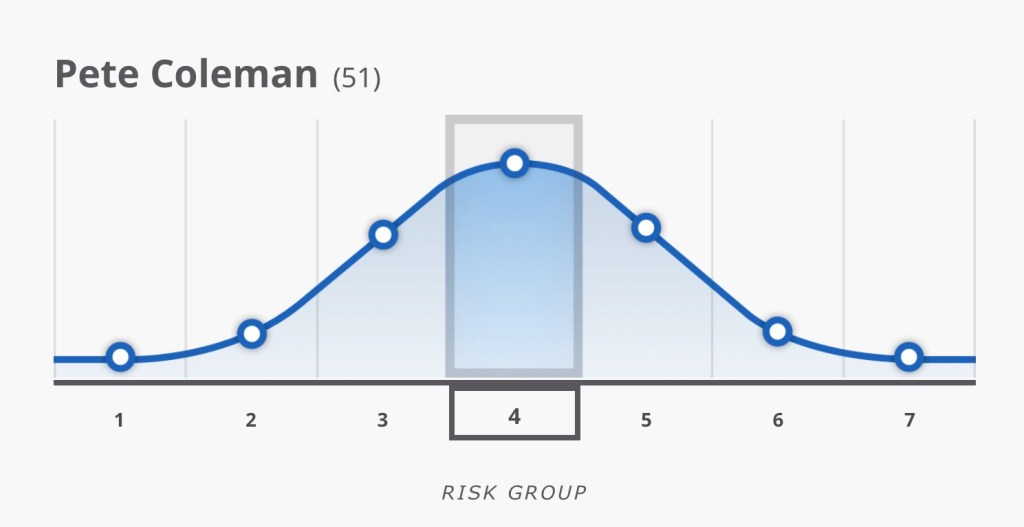

We had a catch up meeting with our financial adviser this week. In preparation we had to fill in risk questionnaires to see if our view of financial risk had changed, and so whether our pension savings were invested appropriately. The result was that I am on the 51st percentile, or to put it another way, boringly average.

I was disappointed with this result. Not because I am disappointed with how risk averse I am. I would not to want to be gambling with my money at a stage when I am retired and no new money is coming in. Nor because I am disappointed with how much I like to take risk. I worked in financial services for most of my career and understand that an element of risk comes with the returns that I think we should be getting from our savings.

But I am disappointed that it is bang in the middle because doesn’t that just make me very boring? I think now that I am retired that is my biggest dread. That I have become a boring old man. As an old work colleague once told me about retirement – my biggest adventure each day would be deciding whether to buy white or brown rolls for my lunch. I don’t think I am quite there yet. For me, my narrowboat life and long vacations are fascinating and I learn new things every day.

But I can see for others that my life must seem really unimportant and boring.

In the UK we have had a pretty volatile week in the markets after what seems like a crazy mini budget, giving away millions in tax cuts, funded by massive borrowing. In a country usually noted for financial sobriety, it has been a shock to feel like a banana republic. This crisis coincided by chance with the six monthly visit from our financial advisor, Neil. We have worked with Neil for about six years. We pay him quite a lot for his advice, You might ask why we would do that, when post retirement, we have reasonably simple finances. No money coming in, and the savings pots not changing very much. The reason we work with Neil may surprise you. We value his life advice as much as his money advice.

When we started working with Neil, his main questions were not about things like our risk appetite and pension valuations. Yes he dealt with all that stuff, and we have done a mix of things with our money. But – the questions were about what we wanted to do with our lives. He would then work to make our money fit our choices. Our answer was that we had always talked about retiring early and owning a narrowboat. He told us that the disappointing thing was that many people have dreams about retirement, but very few actually fulfil them. The temptation of working just a few more years is too high, either to get more money, or because they don’t want to let go of the status work gives them, or simply because of habit.

Around this time, a very good friend passed away suddenly. He was younger than either of us, and it was a shock that reinforced Neil’s advice. If we had this dream, why not follow it. So we bought the boat pretty much immediately. And we put a date in our minds for retirement – end of 2020. I did wonder if having made that decision, work would start becoming boring as I trudged through it to retirement. But in fact it reinvigorated me and my last couple of years working were amongst my most fulfilling and successful. In the final three months I started reducing my hours to get myself ready, and on 2nd January 2021 I retired and we set off on our new adventures.

It was good advice from Neil, and that is still what we get. When we met him this week we were talking about moving house, something we have talked about for a few years. We have prevaricated because we could live anywhere and it has been hard to choose. We seem to be narrowing down on the North West of England but are not sure. Neil’s suggestion is to sell up, rent somewhere where we think we want to live, and take our time to see if it is right for us. With likely falling house prices, we are unlikely to lose. He also told us not to scrimp on what we spend on a new house because it is “just changing asset classes”.

Good advice. Mind you, after this week’s mini budget, maybe we would be better off living outside the UK. What do you think?

I consider myself quite well off. I was lucky enough to be able to retire when I was 56 and can afford to spend much of the year travelling on our narrowboat. I am clearly not oligarch wealthy but I can afford not to worry too much about money. But this week we have been navigating the Thames from Oxford south, passing small towns such as Wallingford, Goring and Pangbourne. I have realised that there are so many really rich people living here, that by comparison I am a pauper.

A house

The houses are often very large and ornate, with expensive boats, sometimes in their own boathouses, and large gardens rolling down to the river. George Michael’s house is in Goring and recently sold for £3.4m – and it is a relatively small house.

A boathouse

Seeing so much opulence has given me a different view of wealth. Am I jealous? Maybe a little. But we once lived in a large mill owner’s house in Yorkshire so we have done that. It cost a fortune to maintain, and most of the time we did not use most of the rooms. I could have earned more in my working life. Certainly I could have worked for longer and accumulated more wealth.

But that is not what life is about for me. Working till I am 75 and then crashing with a heart attack. What makes me rich is not the money we have. It is the time we have. Mandy, the dogs and I can enjoy life at a slow pace, see places we have never seen, meet people we have not seen in too long, make new friends along the rivers and canals.